This is the first post of a multi-part series of common economics misconceptions. Economics may be the ‘gloomy science’, but it also tends to be a counterintuitive one as well. The media, often ignorant about the intricacies of macroeconomics, unwittingly spread these fallacies to the general public, as well as regurgitated by politicians who, like the media, also tend to be naive about economics.

The first part is about the fallacy of composition as it pertains to budget deficits in America. The fallacy of composition is the mistaken belief that a large system can be generalized by one of its smaller components, or the belief that a smaller system is representative of the bigger one it belongs to. While it may be prudent for a household to save money (run a surplus), it may not be so for a country. In this case, the smaller component is the household, which is a part of the bigger system (the state). A state, unlike a household, is better suited to running deficits due to these key differences:

A state can roll over its debt in perpetuity, whereas for a household debt is discharged upon death of the debtor.

A state can print money; a household obviously cannot.

A state, particularly in the case of reserve currency status, has much cheaper borrowing costs than an individual. The US government can borrow 30-year debt at just 3% a year and 10-year debt at less than 2%; meanwhile credit card debt for an individual can run as high as 20-30% a year. Japan and Germany are other examples of countries that have very cheap borrowing costs due to reserve currency status. The best an individual can hope for is to have a high credit score.

This is why, as I’ve explained numerous times, contrary to the debt doom and gloom in the media, the national debt may not be such a big of a deal. But doesn’t mean we should squander our reserve currency status by spending indiscriminately. Emerging markets like Brazil and Turkey, on the other hand, do not have reserve currency status, and this a major reason why they pay much higher interest on their debt and are at a much higher risk of defaulting.

But back to the topic of surpluses, why are they not so great? Remember the Clinton surplus, widely touted by the media as the crowning economic achievement of the Clinton administration? What the liberal media won’t tell you is that the economy actually entered a recession in 2001 on it, which is why the recession is sometimes mistakenly called the ‘Bush recession’, but it began in the late ’90s at the end of the Clinton’s second term. That’s right… ‘the great Clinton surplus’ may have caused a recession. The reason why is explained in an excellent article by L. Randall Wray, Teaching the Fallacy of Composition: The Federal Budget Deficit. This should be required reading for anyone who wishes to better understand macroeconomics:

We can divide the economy into 3 sectors. Let’s keep this as simple as possible: there is a private sector that includes both households and firms. There is a government sector that includes both the federal government as well as all levels of state and local governments. And there is a foreign sector that includes imports and exports; (in the simplest model, we can summarize that as net exports—the difference between imports and exports—although to be entirely accurate, we use the current account balance as the measure of the impact of the foreign sector on the balance of income and spending).

At the aggregate level, the dollar spending of all three sectors combined must equal the income received by the three sectors combined. Aggregate spending equals aggregate income. But there is no reason why any one sector must spend an amount exactly equal to its income. One sector can run a surplus (spend less than its income) so long as another runs a deficit (spends more than its income).

Historically the US private sector spends less than its income—that is it runs a surplus. Another way of saying that is that the private sector saves. In the past, on average the private sector spent about 97 cents for every dollar of income.

Historically, the US on average ran a balanced current account—our imports were just about equal to our exports. (As discussed below, that has changed in recent years, so that today the US runs a huge current account deficit.)

Now, if the foreign sector is balanced and the private sector runs a surplus, this means by identity that the government sector runs a deficit. And, in fact, historically the government sector taken as a whole averaged a deficit: it spent about $1.03 for every dollar of national income.

Note that that budget deficit exactly offsets the private sector’s surplus—which was about 3 cents of every dollar of income. In fact, if we have a balanced foreign sector, there is no way for the private sector as a whole to save unless the government runs a deficit. Without a government deficit, there would be no private saving. Sure, one individual can spend less than her income, but another would have to spend more than his income.

While it is commonly believed that continual budget deficits will bankrupt the nation, in reality, those budget deficits are the only way that our private sector can save and accumulate net financial wealth.

Budget deficits represent private sector savings. Or another way of putting it: every time the government runs a deficit and issues a bond, adding to the financial wealth of the private sector. (Technically, the sum of the private sector surpluses equal the sum of the government sector deficits, which equals the outstanding government debt—so long as the foreign sector is balanced.)

Of course, the opposite would also be true. Assume we have a balanced foreign sector and that the government runs a surplus—meaning its tax revenues are greater than government spending. By identity this means the private sector is spending more than its income, in other words, it is deficit spending. The deficit spending means it is going into debt, and at the aggregate level it is reducing its net financial wealth.

Here is another excellent article that explains why surpluses may not be desirable, with computer-generated simulations of how surpluses can cause the economy to shrink and private debt to soar.

This related to Modern Monetary Theory:

In any given time period, the government’s budget can be either in deficit or in surplus. A deficit occurs when the government spends more than it taxes; and a surplus occurs when a government taxes more than it spends. MMT states that as a matter of accounting, it follows that government budget deficits add net financial assets to the private sector. This is because a budget deficit means that a government has deposited more money into private bank accounts than it has removed in taxes. A budget surplus means the opposite: in total, the government has removed more money from private bank accounts via taxes than it has put back in via spending.

Therefore, budget deficits add net financial assets to the private sector; whereas budget surpluses remove financial assets from the private sector. This is widely represented in macroeconomic theory by the national income identity:

G − T = S − I − NX

where G is government spending, T is taxes, S is savings, I is investment and NX is net exports.

While people talk nostalgically about the ‘go-go 90s’, beneath the veneer of rising stock prices there may have been rust, which I explain in greater detail in the widely-cited dyseconomics article. The bull market and economic expansion that began in the early 80’s during Reagan’s tenure was running on fumes by the late 90’s, as PE ratios were very high, GDP growth had slowed, and corporate profit margins were falling.

You can see above how corporate profits began to shrink in the late 90’s, culminating in a recession by 2001 and, of course, the 911 attacks did not help the situation. In 1993, Clinton raised taxes, which many years later may have caused the recession, as the government slowly began to suck money from the private sector to fatten its own balance sheet, creating this ‘surplus’ that looked good on the 2000 campaign trail for Al Gore, but was draining the life out of the economy. Then Bush stepped in, lowering taxes and boosting other spending (which I know many Republicans now regret), ending the recession. Also the post-2002 BRIC boom helped, which allowed the fed to keep rates lower longer than usual, as well boosting the economy through exports.

As you can see above, by running a surplus in the 90’s, the government was, essentially, taking from the private sector, which could explain why the economy recovered when taxes were lowered under Bush. By 2000, when the economy entered recession, private sector balances hit multi-year lows while government balances were at record highs.

So the question is, if deficits are good and surpluses are bad, why did this not work in Greece and Japan? Technically, we can’t assume beyond all reasonable doubt that Japan’s policies failed; had they done nothing, things could be much worse than they are now. Likely, things would have been worse, but it’s impossible to know. Japan, like America has large economy and reserve currency status, so they pay very little interest on their debt. Greece has a much smaller economy, making it hard for to find buyers of their debt, whereas America always has buyers, the result being much higher yields for Greek debt due to the increased risk of default and lack of buyers. Also, how the money is spent is also important. Spending for low-ROI programs like welfare, pensions, and disability will not grow the economy as much as spending on high-ROI programs like tax cuts, technology start-ups, gifted education, and defense. Relative to GDP, Greece’s ratio of public pension payments is higher than America or the rest of the European Union.

What about crowding out? The evidence suggests that this is not a problem: interest rates are lower than ever in spite of record-high deficit spending in the US and other developed countries:

According to American economist Jared Bernstein, writing in 2011, this scenario is “not a plausible story with excess capacity, the Fed funds [interest] rate at zero, and companies sitting on cash that they could invest with if they saw good reasons to do so.”[5] Another American economist, Paul Krugman, pointed out that, after the beginning of the recession in 2008, the federal government’s borrowing increased by hundreds of billions of dollars, leading to warnings about crowding out, but instead interest rates had actually fallen.[6] When aggregate demand is low, government spending tends to expand the market for private-sector products through the fiscal multiplier and thus stimulates – or “crowds in” – fixed investment (via the “accelerator effect“). This accelerator effect is most important when business suffers from unused industrial capacity, i.e., during a serious recession or a depression.

I also agree that fears of crowding-out are overblown and unlikely to materialize in terms of lowered GDP growth or stagnation due to the private sector being ‘crowded out.’ But a 2010 Mercatus article In the Long Run, We’re All Crowded Out cautions otherwise:

When government borrows to finance its spending, it competes with private entrepreneurs who are borrowing to finance their own activities. Capital used by the government is capital that cannot be used by private businesses. Moreover, when government borrows, competition in the market for loanable funds increases, raising the price of borrowing, or the interest rate, for private investors. For firms, this means an increase in the cost of doing business. Companies and projects that would have otherwise been profitable are no longer able to be so at the higher interest rate.13

Yeah, but government spending also flows into the private sector, too, such as defense contracts or to fund tax cuts. And it’s not like the government and the private sector are competing for the same capital: the U.S government issues treasury bonds; corporations issue corporate bonds. The latter have a higher interest rate and risk. Risk-averse lenders will buy the former. The only way for this to be broken would be for government bonds to have a higher yield than corporate bonds of the same duration, but this never happens. Given that 10 years have elapsed since the publication of the aforementioned article, we can assess the prescience of the authors’ warnings. The empirical evidence since 2010, when the article was published, is that in spite of record-high deficits and deficit spending, interest rates are lower than ever, and that private sector is healthier than ever in terms of record-high profits for S&P 500 companies and stock prices, and the US economy, by almost every metric, is stronger than ever.

What about reduced GDP?

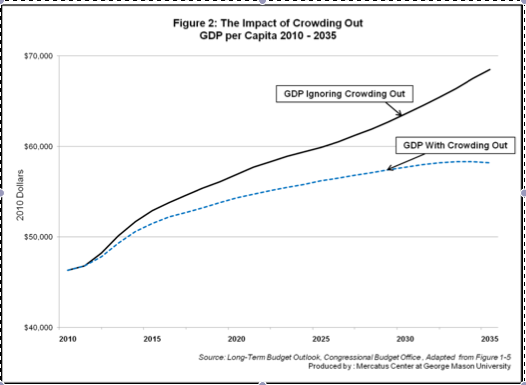

The CBO has also estimated the cost of crowding out over the long run (see figure 2). By their estimate, crowding out will reduce inflation-adjusted gross domestic product per person by 6 percent in 2025 and by 15 percent in 2035.25 For the economy at large, this means an economic cost of $1.2 trillion in real lost economic activity in the year 2025, more than the cost of the wars in Iraq and Afghanistan combined. For individuals, this will mean lower incomes and less opportunity.

That, too, hasn’t panned out. GDP per capita is doing better than ever, in agreement with the black projection. According to data by the World bank, 2018 US GDP per capita in 2010 dollars is $55,000/person, right in line with the projection excluding crowding out.

Recent evidence suggests the opposite: a crowding-in effect:

A new working paper by Enrico Moretti, John Van Reenen, Claudia Steinwender, from the economics departments of the University of California, Berkeley and MIT, and the MIT Sloan School of Management respectively, explores one particular segment of federal spending — defence research and development — and its effects on private sector R&D expenditure.

In contrast to expectations, the paper finds that public sector R&D expenditure — whether directly or via subsidies — actually leads to an increase in private sector spending in R&D. A “crowding-in effect”, if you will.

What about high inflation due to deficit spending? That too hasn’t happened. In spite of record-high deficits under the past three presidents, interest rates and CPI are very low. Had someone sat out of the stock market in 2009 over concerns about the national debt, they would have missed out on arguably the biggest stock market boom ever, missing out on hundreds of percent of real gains. America having $20 trillion dollars of national debt that will never be paid back in full but rather just rolled over in perpetuity, does not stop individuals from realizing real gains in wealth by investing.

Regarding the national debt, what matters more is not the absolute amount of debt but debt relative to GDP and interest paid on debt relative to GDP. Those metrics are more favorable now than they were decades ago in spite of more debt overall. Also, 1/3 of the debt the US owes to itself, as opposed to private and foreign investors. Debt to GDP was higher in WW2, and Japan has even much more debt relative to GDP yet has not encountered problems. We’re seeing a race to zero (and below) globally in regard to interest rates for the largest and most developed of economies. There is so much capital and so few alternatives besides low yielding debt. As bad as Northern Europe may seem regarding immigration, as as dysfunctional as the US is in regard to politics, it’s still way better than the alternatives such as Brazil, Turkey, or Russia.

An important and overlooked factor for why Wiemar Republic hyperinflation is much less of a concern for the US than emerging markets, is that the US government issues debt in the same currency is uses to repay it and the value of such debt is assessed against. This is explained in more detail in the post Explaining the national debt: why I’m not concerned.

This seems to affirm the MMT view of economics as being the more correct one, even if not necessarily perfect or optimal (I think that incurring a bunch of debt for universal healthcare or student loan forgiveness, may not be the best use of capital. My approach is more on the supply-side.). The overall trend has been that high deficits are compatible with a strong overall economy and a strong, profitable private sector.

Related:

Economics Myths, Part 2: America Is In Decline/The Dollar Is Weak