Over the past few months, the legendary investor Warren Buffett has been showered with adulation by the media for raising cash in 2024, having seemingly anticipated the downturn of 2025. Note: We’re talking Buffett’s company Berkshire Hathaway, not Buffett himself, although these are often used interchangeably. From Business Insider, The internet is in awe of Warren Buffett’s perfectly timed cash-out:

Warren Buffett is being praised for paring Apple and stacking cash before the market correction. Social media is full of Buffett quotes about slumping stocks and memes featuring the investor. Buffett’s Berkshire Hathaway sold a net $134 billion of stocks in 2024 and built a record cash pile.

Given that the S&P 500 has fallen 5% since peaking in February 2025 over fears of tariffs by the Trump administration, Buffett’s timing appears especially prescient. Or is it? Looking deeper paints a different picture. So, although Buffett’s timing looks good now, zooming out, suggests otherwise.

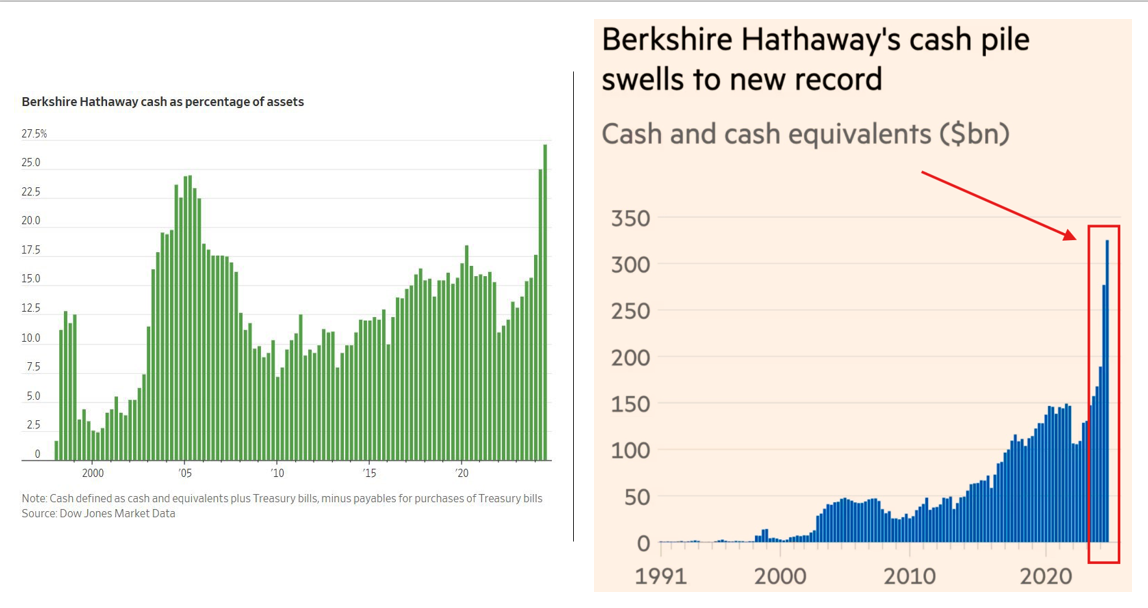

Buffett has been raising cash for a long time. Buffett’s cash pile has grown considerably since 2009, when stock market bottomed during the global financial crisis. As the S&P 500 has surged, Buffett’s cash pile has only grown:

Since bottoming on March 2009, the S&P 500 has gained 700%, possibly surpassing even the bull markets of the ’90s and ’80s in terms of gains:

If anything, this suggests the opposite of good timing, which is that by being too conservative and raising cash against the backdrop of such a strong bull market, Buffett left a lot of money on the table. Had he had invested Berkshire’s cash in the S&P 500 instead, instead of ‘only’ having $325 billion, he could conceivably have a trillion dollars or more.

Buffett doubled Berkshire’s cash position in 2024 from $150 billion to $300 billion:

In 2024, the S&P 500 surged 25%, on top of a 26% gain in 2023. The $125 billion in cash he had accumulated by late 2017, had he invested in the S&P 500 instead, would be worth $250 billion today, including dividends and after factoring in the 2025 selloff. So that is $125 billon left on the table.

To be vindicated–that is–to negate the opportunity cost of having stayed in cash from 2018-2024 during such a strong bull market, would require that the S&P 500 fall about 34% from its 2025 peak, which is a long way from the 5% it has already fallen this year.

I calculated this by setting up the equilibrium equation: \(\left( \frac{5500}{2700} \right) (1-n) \cdot 150 – 150 = 150n\)

The LHS of the equation represents the opportunity cost of having kept roughly $150 billion in cash instead of investing it in the S&P 500 from 2018-2025, which rose from 2700 to 5500 in that period. The RHS represents how much he will have saved by having raised an additional $150 billion at the market top in late/early 2025. The market falling lowers his opportunity cost. Where these two intersect is the ‘break even’ point. This requires about a 34% correction from the 2025 peak.

This does not look promising. Even in 2022 or during Covid, the S&P 500 only fell 20-25%, and only briefly. For Buffett to be vindicated would require a repeat of something like 2007-2009 or 2000-2002, in which the S&P 500 fell over 50%, for a much more protracted period.