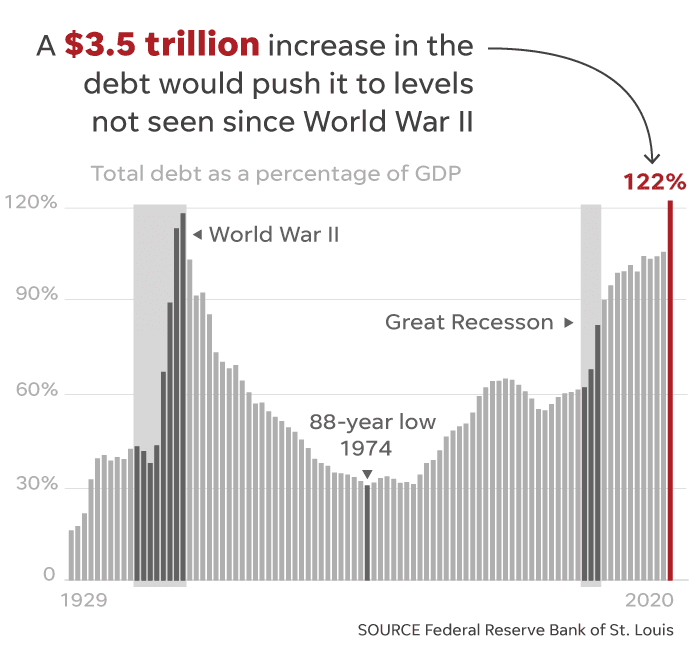

Due to Covid, the national debt has swelled to levels never before seen, at $26 trillion, and debt to GDP also made new highs, surpassing the highs of WW2:

People are wondering, “Is this sustainable?” “Will income taxes have to rise?” “Will there be hyperinflation?”” Will the dollar collapse?”

In short: yes, no, no, and no.

In spite of surging deficits over the past 20 or so years, since the Iraq and Afghanistan wars and the Bush tax cuts, the 2008 financial crisis, and the 2020 Covid bailouts, the US economy has continued to defy all predictions of debt crisis, currency collapse, and hyperinflation. CPI just refuses to budge above 2%, the US dollar is at near multi-decade highs against currencies such has the Euro and Pound, and yields on Treasury bonds keep falling to lows never before imagined were possible. A 10-year treasury bond yields just .6%–a 90% reduction from the late ’90s and early 2000s.

A common objection to such deficit spending is that taxes will have to go up to pay for it. But income taxes have been falling for decades in spite of surging deficits. It is more like it is paid by bond holders at near 0% yield, than out of the pockets of tax payers. If the economy is growing at 2% a year and interest on the debt is 0-.5%, then it’s possible to grow the debt away by expanding the total size of the tax base rather than raising taxes. The payment is always being deferred, as the debt is rolled over in perpetuity, so tax payers may never have to actually pay more in taxes. I think globalization, multinationals, near-0% interest rates ,and the US dollar being the #1 reserve currency in the world, make it possible for the US to serve very high levels of debt without the typical/textbook consequences that may arise from so much debt. This ties in with MMT. MMT only works in the US (and possibly also Japan , Germany, and UK) for this reason. MMT would not work in smaller, developing countries, because printing money leads to a direct loss of wealth and increased debt burden due to currency decline relative to the US dollar and the currency said country borrowed against.

But won’t the bill come due? A national debt–especially for a dominant economy with reserve currency status such as the US–is not at all like a gambling debt or credit card debt. Some mistakenly assume the rules of household and business budgets apply to federal budgets , when the two cannot be more distinct. Individuals must borrow at a high interest rate but the US can borrow at close to nothing and print moeny to pay its debts in the same currency it is dominated in. Imagine owning someone money at .5% interest and being able to print money to pay the interest and the creditor not demanding more money to compensate for the inflation of currency.

The question becomes, how much money can the US print before inflation and other problems arise, and the answer is probably “a lot more than originally believed.” The fact that in response to Covid, about $2 trillion in stimulus have been given out to individuals and businesses without any appreciable bump in inflation, shows we’re probably nowhere near that threshold. The CAREs packages and related programs are effectively mini-versions of a UBI but inflation has not budged in terms of CPI, although it has surged in terms of healthcare and tuition costs, rent, insurance, daycare and a bunch of other services [although this apparent bifurcation of inflation has been observed for a long time, well before Covid]. This inflation is negated to some degree by deflation for tangible goods such as electronics, food, and clothes.

There may be no theoretical limit of spending if the US can generate real GDP growth from such spending. If the US govt. can borrow at 0% and that money indirectly goes to Amazon and other innovative tech companies in the form of consumer spending, which generates real growth from Amazon investing the money in business operations, then the US govt can come out out ahead and grow its debt away: That is already the case now, in which the US is paying around .5%/year to service new debt despite GDP forecasts of 2-3%/year. As the economy recovers from Covid, interest rates and bond yields will take forever to go back up, if they ever do. Of course, interest rates may rise, but the trend is for rates to keep falling. Also you cannot have inflation if wealth is demonstrated in dollars. What I mean is is, hyperinflation is usually an event that occurs in the context of a second more stable currency. This is why currency devaluation is a real problem for small economies but much less so for the US, because it means that wealth is also being destroyed, so the country becomes poorer and things can get bad.